Mortgage Interest Rates Are Up! Are Home Buyers Losing Ground?

Posted March 24, 2018 in Special Features

It’s not new news that mortgage interest rates have been on a steady rise over the last year or more. According to Freddie Macs 2018 Primary Mortgage Survey1 the 30 year fixed rate has increased about one-half of one percent (1/2%) since January 2018 alone!

The Mortgage Bankers Association2 also has made their rate forecast into this year and 2019-2020. The consensus is that rates are expected to continue to increase. But how fast? How high? That has yet to been seen, but the MBA reports (sourcing Freddie Mac, Federal Reserve, MBA) that we can expect to see interest rates in the mid-5%’s into 2019 and 2020.

Historically speaking3 a 5 ½% interest rate is a great rate! The 1980’s, 1990’s or even early to mid-2000’s versus rates today shows we’re still sitting pretty good! In the 1980’s homebuyers were faced with borrowing money at a rate up to 17%. In the 1990’s, a mortgage seemed to be a great bargain even when they pushed 10%, and in the early-mid 2000’s we saw homebuyers borrowing at rates up to 8%. Mortgage rates for a 30-year mortgage finally took somewhat of a free-fall in 2012 when the average was about 3.66% for a 30-year fixed loan.

So for many homebuyers in today’s market – especially the first-time homebuyer or the move-up buyer going from their first home to their next, the 4+% rate that we’re seeing today or even the 5.5% interest rate that might be looming ahead may seem shocking.

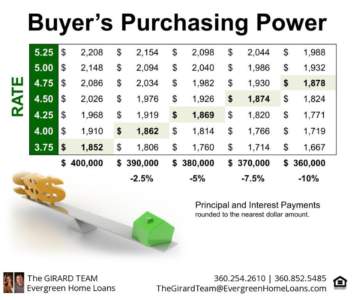

When you compound increased interest rates with the appreciation of home prices, buyers may feel a double whammy when shopping for a home. Here’s an example:

A $400,000 home loan at last year’s rate of 3.75% will now cost the home buyer an additional $234/month with a rate of 4.75%, or if their budget won’t allow for the higher payment they have instead lost about 10% in their purchasing power, having to shop for a lower priced home or bringing in more down payment to keep their loan at $360,000.

Let the numbers speak for themselves. Historically speaking it is still a great time to buy a home. Rates are still at historical lows, maybe not as low as we’ve seen, but still good! If you’re on the fence, keep in mind that procrastination could be costly, a difference of hundreds of dollars per month more in house payment because of a rate increase alone. Not counting the chances that home prices are expected to continue to rise.

Innovative programs while you house hunt, like the Lock and Shop program from Evergreen Home Loans locks in your interest rate for 60, 75 or 90 days with no adjustment to your fee while you shop. By staying informed and working with an experience real estate agent and mortgage professional, you can stay a step ahead in a changing market.

Leslie Girard is the branch manager for the Southwest WA area branches at Evergreen Home Loans. She lives in Vancouver with her 2 grown children and 1 grandson.

Sponsored by The Girard Team, Evergreen Home Loans

(360) 254-2610 | (360) 852-5485

TheGirardTeam@EvergreenHomeLoans.comLeslie Girard, NMLS #58461

Sources:

- Freddie Mac 2018

- MBA Economic and Mortgage Finance Outlook – February 2018

- com/pmms/pmms30.html

© 2018 Evergreen Home Loans is a registered trade name of Evergreen Moneysource Mortgage Company® NMLS ID 3182. Trade/service marks are the property of Evergreen Home Loans. All rights reserved. Licensed under: Alaska Mortgage Broker/Lender License AK3182 and AK3182-1; Arizona Mortgage Banker License 0910074; California Licensed by Department of Business Oversight under the California Residential Mortgage Lending Act License 4130291; Idaho Mortgage Broker/Lender License MBL-3134; Nevada Mortgage Banker License 3130; Oregon Mortgage Lending License ML-3213; Washington Consumer Loan Company License CL-3182.